Shkruar nga Pamfleti

Shkruar nga Pamfleti

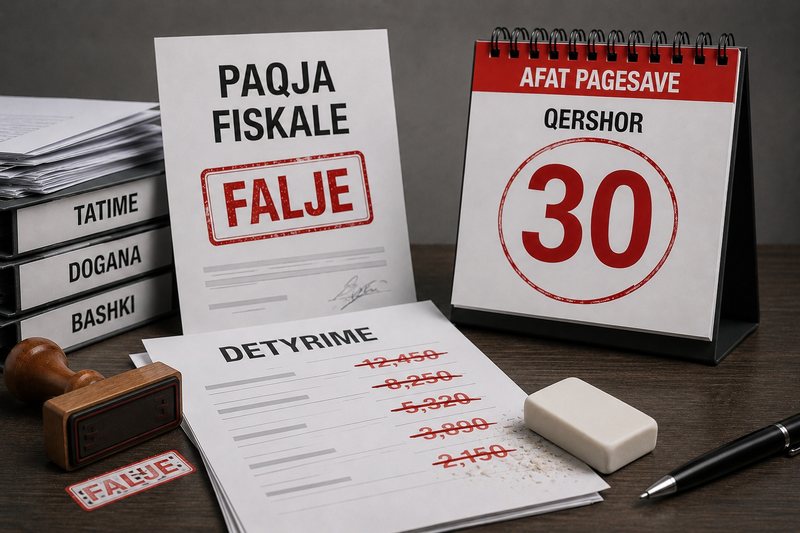

Following the entry into force of the guidelines for the implementation of the "Fiscal Peace" law and the one for the forgiveness of tax, customs and local government obligations, experts warn that the short deadlines for application and payment may create difficulties for businesses and the tax administration.

Legal auditor Bujar Bendo emphasizes that the legal guidelines were approved two months late, while the deadlines for their implementation are very limited.

"From the beginning, I would like to emphasize a disproportion in the time of the effectiveness of administrative acts. The Ministry of Finance's instruction on the Fiscal Peace agreement was issued with a delay of two months. Within this same time limit, a tax administration instruction was also issued. The latter has subjectively determined a tight deadline for the entry into force of the law itself. In practice, it will create many problems with the implementation of the process," he claims.

Accountant Sotiraq Dhamo also estimates that businesses have very little time to benefit from the forgiveness of obligations and fines.

He cites as an example the period June 5–30, 2026, when entities must apply, make payments, and submit relevant documentation within 25 days.

Accountant Dhamo suggests that the tax administration should extend the deadline for making payments to June 30, 2026.

"I note that the time to apply for the cancellation of obligations and fines is also very short, as the instructions have also been issued late. So, the right to request or cancel obligations and fines for the years 2015–2024 begins on June 5, and to forgive fines, e.g. if 50% of the obligation is paid, the payment must be made within June 30. So only 25 days to recognize and implement this legal right. Perhaps this deadline of June 30 should be extended by law," says Dhamo.

According to the calendar published by the General Directorate of Taxes, applications in the "e-Filing" system for the Fiscal Peace Agreement started on May 15 and end on June 5, 2026. Until June 30, entities must submit the signed agreement, pay taxes for re-declarations and upload corrected financial statements.

Also, by June 30, 2026, businesses must pay 50% of the obligations for the period 2015–2019 to benefit from the forgiveness of the remaining part, while the final deadline for other payments and the forgiveness of penalties ends on December 31, 2026. By June 30, the deadline for submitting undelivered declarations for the periods until 31.12.2024, to benefit from the forgiveness of fines for late declarations.

In addition to taxes, the law on debt forgiveness has also begun to be implemented by the customs administration and local governments.

The General Directorate of Customs previously announced that the deadline for the partial forgiveness of unpaid customs duties for the period from January 1, 2015 to December 31, 2019, specifically at the rate of 50%, is until June 30, 2026.

"If you pay by June 30, 2026, you will receive forgiveness of up to 50% of the principal and 100% of fines and late interest," the customs administration explained.

The General Directorate of Taxes and Tariffs of the Municipality of Tirana also announced that for unpaid obligations to the local government for the period January 1, 2015 - December 31, 2019, two alternatives for benefit are foreseen: payment of 50% of the principal by June 30, 2026, with the rest forgiven, or payment of 75% of the principal by December 31, 2026, with the rest forgiven. In both cases, all fines and late fees are forgiven.

Categories of liabilities that benefit from deletion/extinguishment

Outstanding liabilities as of December 31, 2014

Unpaid liabilities pertaining to tax periods up to 31.12.2014 are completely erased, including fines and late interest. The principal liability for social security and health insurance contributions is not forgiven.

Outstanding liabilities for the period January 1, 2015 – December 31, 2019

-50% of the principal obligation is canceled, if the remaining 50% is paid at once from 10.06.2026 to 30.06.2026;

-25% of the principal obligation is waived, if the remaining 75% is paid from 10.06.2026 to 31.12.2026. In both cases, fines and late interest are completely waived. In both cases, fines and late interest are completely waived.

Outstanding liabilities for the period January 1, 2020 – December 31, 2024

Fines and late fees are waived provided that the tax for the relevant period is paid in full (100% of the principal) from 10.06.2026 to 31.12.2026./Monitor

Lini një Përgjigje